Enabling the emergence of global Ecological Assets

Carbon markets are just the beginning when it comes to this new asset class

Overview

Pricing negative externalities has always been tricky. The science is there that climate change has a net negative effect on the well-being of the planet, but imagining the cost of an invisible gas is a tricky thing to drill into the public conscience.

What people can imagine, however, are savings. How much could have been saved or what were the costs of extreme weather conditions?

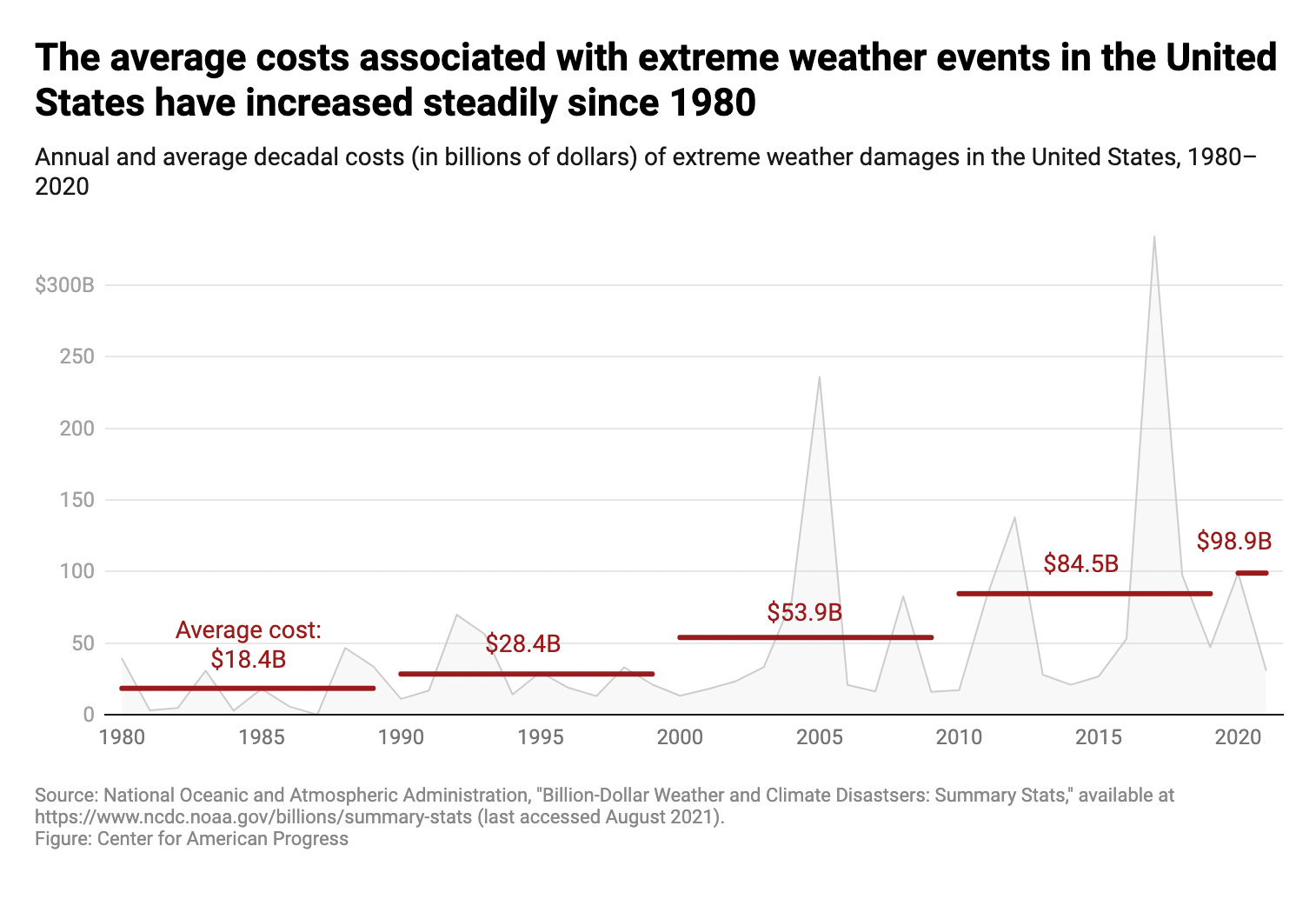

The graph shows the average cost for the US alone, a clearly increasing trend over the past decades. Supply chains are also impacted by extreme weather conditions, characterised by increased frequency of disruption to the global movement of goods. Suppliers reported to the CDP in 2020 that such impacts could result in additional costs of $120 bn to buyers over the next 5 years. These costs will eventually get passed on to consumers, adding to inflationary pressures worldwide. A green transition is bound to fuel a persistent ‘higher than wanted’ inflation as new money is created to finance the transition while carbon allowances continue to decrease thereby increasing carbon prices. Assuming demand stays constant, prices of carbon intensive products across the board will rise. In any case, both tackling climate change and not tackling climate change will add to inflationary pressures, the former however is an investment in the future that will pay off and include many positive externalities while the latter will be a constant fire fighting exercise whose cost increases exponentially with only more negative externalities in its path.

So we can imagine how our pockets are hurt by climate change. We could save more by having a healthier global ecosystem. The transition to a more sustainable future will be costly; yet the emergence of a global carbon market represents a new opportunity as an asset class that is bound to grow in size and volume as companies and countries find themselves cornered the longer they wait to take action to net zero.

Carbon Markets

The global carbon market is divided into two categories:

The Compliance Carbon Markets (CCM), which is the biggest one by far such as the EU ETS

The Voluntary Carbon Markets (VCM).

The CCM is a mandatory regulated scheme whereby businesses whose emissions exceed a defined threshold (allowance), or who operate in emission heavy industries, are required to obtain a credit for each CO2 that they emit annually. These thresholds decrease over time making it more expensive to emit the same amount of carbon tonne.

Businesses who reduce emissions can sell their excess carbon credits to those that have exceeded their allowances. Matter of fact Tesla has been making significant money, roughly $429 million on average over the last five quarters, only through carbon credit sales to other automakers.

The VCM on the other hand, is a market that is created by any organisation or individual that wants to offset their greenhouse gas emission on a voluntary basis. Most businesses would purchase credits from the VCM to fit into their Corporate Social Responsibility (CSR) targets. These offset come from projects around the world that remove or avoid a tonne of CO2.

Despite the existence of standard setting bodies in the VCM market, it remains a heavily fragmented and mispriced market being handled by brokers. The fragmentation arises not only due to a lack of standardisation but also due to data quality behind these projects being opaque, making it difficult to establish whether a CO2 tonne removed is actually a tonne of CO2 removed or avoided.

So, we have a regulated (mostly EU) market that aims to cap and trade by making companies pay for exceeded emissions and a fragmented voluntary market that is inefficient and somewhat reliant on social pressures for companies to do good. Both complement each other, however, in growing the size of the market. Wood Mackenzie, a global energy research group, estimated that the market could grow to $22 trillion by 2050. It’s also somewhat ironic that Trafigura, one of the biggest oil traders, has set up a global carbon trading desk. Carbon is officially a commodity.

Size of Market

CCM

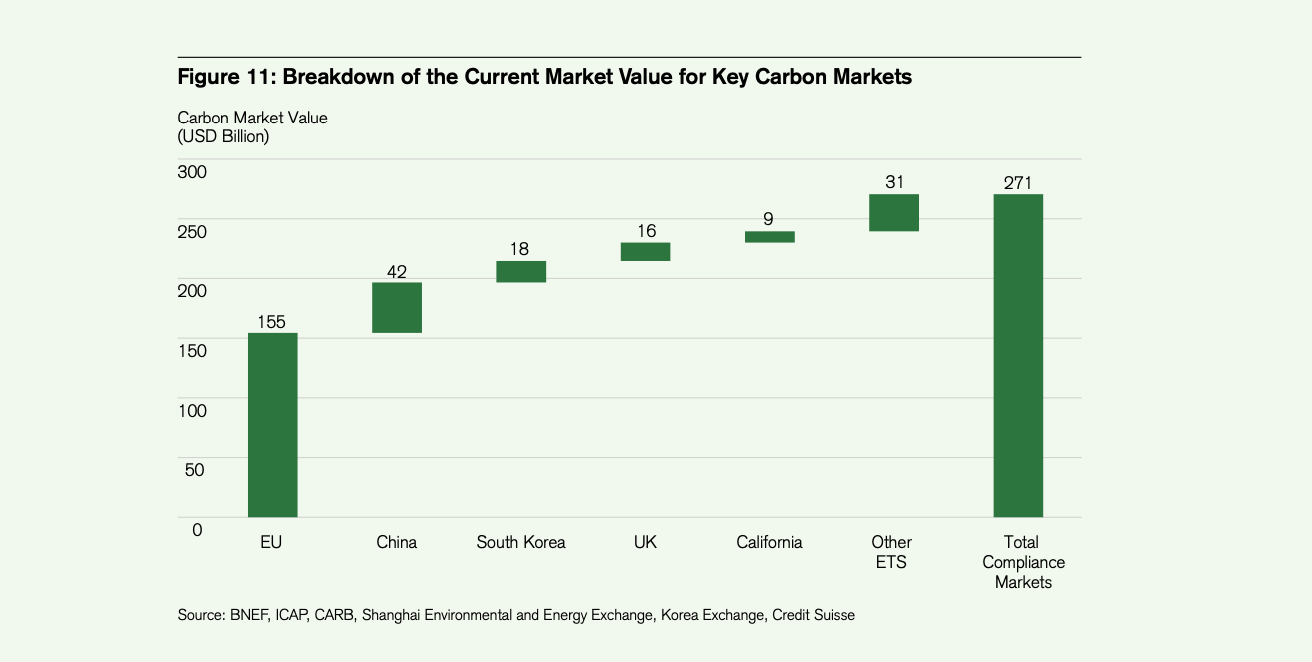

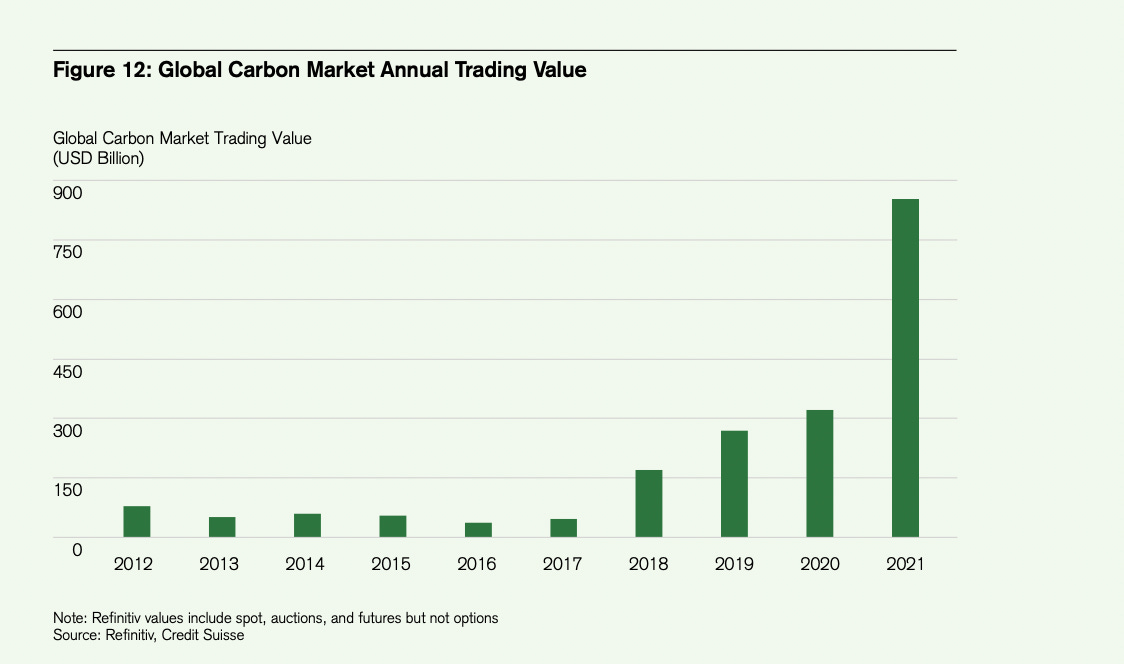

The global trading value of carbon markets reached $851B in 2021 with the market value totaling around $270B. The EU ETS accounted for roughly 90% of trading value as it has become the most liquid and well-established market. Carbon prices in the EU ETS are trading at 80EUR/ton, however the global market weighted average price is closer to $28/ton. This is due to China’s National ETS accounting for over 50% of emissions in the CCM scheme, which are yet trading at just $8.5/ton (YE21)

VCM

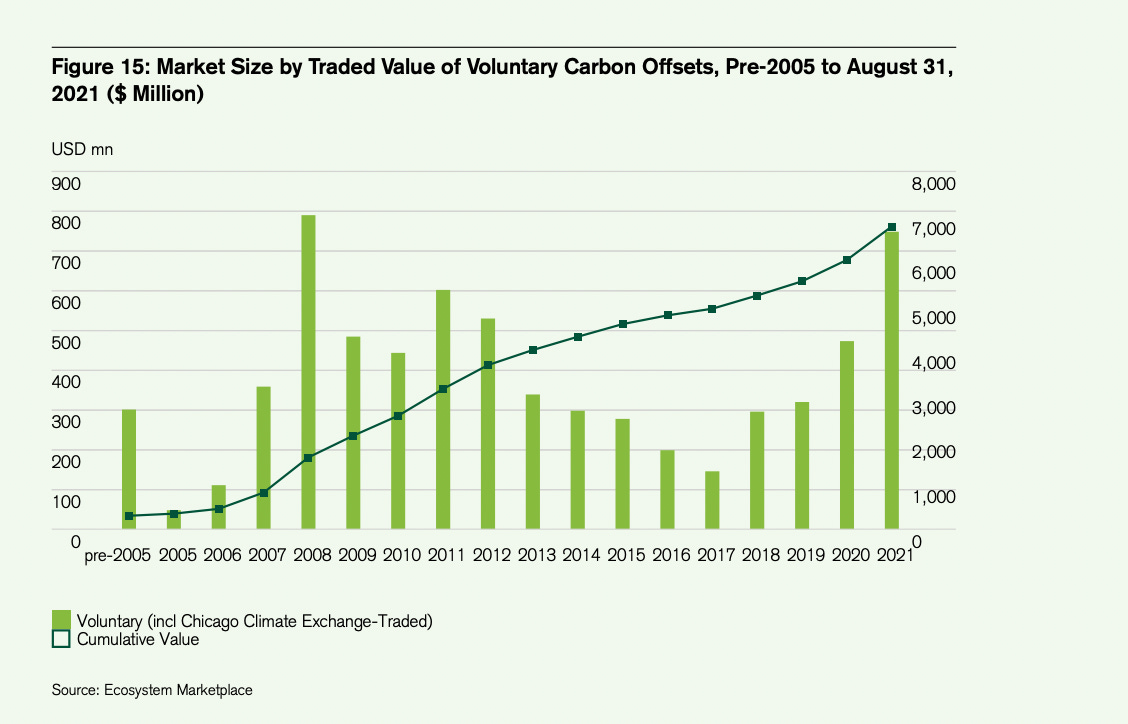

The VCM is much smaller in size with a trade value of around $750M to $1B but also growing. The Taskforce on Scaling VCM, headed by Mark Carney, projects demand for carbon offset projects to reach 1-2 GtCO2 (billion tonnes) by 2030 and 5 GtCO2 by 2050. The price of this demand will depend on the quality of credits, currently ranging from mid single digits to over $200/ton.

The bigger picture

Thinking about carbon markets as just a new asset class, however, misses the point. What these schemes are trying to reward is an ecological state. One with less pollution and less destruction of ecosystems.

The financial system is actually good at rewarding behaviours, provided they can be measured. The carbon market is proving that we can reward decarbonisation.

If we can transparently measure and collect data on other states and ecosystems, there is a way to incentivise creation and regeneration rather than destruction and deforestation. Blockchain technology allows us to not only register data transparently but also tokenise it and thereby price ecological assets.

We must have a way of measuring and accounting these assets, however.

Enter Regen Network

The Regen foundation is working towards creating a balance sheet for Earth.

“For market-driven solutions to achieve regenerative outcomes, full ecological accounting must be available for the private and public sectors.” Regen Whitepaper

There is no one size fits all when it comes to accounting for the state of the earth. Regen is not looking to become the global authority on carbon measuring. Rather it is about providing the tools and infrastructure necessary to carry out these tasks.

The team at Regen have built an architecture that allows for anyone to create their own methodologies within the registry app, these need to be approved however, by the community and the scientists involved. Such an architecture allows other organisations and Regen to collaborate and create different credit classes (EcoCredits) not just ones related to carbon, ultimately making Regen an ecological asset issuance system on a transparent blockchain.

The Regen Registry consists of three main components:

The Regen Ledger

The blockchain infrastructure storing all claims made on ecological state.

The Regen Registry app

The front-end application allowing stakeholders to register projects, buy and sell credits on the marketplace and engage in network governance.

The Regen Registry Guide

Outlines the process by which stakeholders can engage in the creation of new methodologies and issue EcoCredits.

Tying this to the off-chain world we still have the oracle problem. On this front Regen is using multiple sources to verify claims about an ecological state such as IoT sensors, user input, satellite imaging and public geographic information systems (GIS). The data is then timestamped and stored on a data layer like IPFS.

The Regen Foundation will develop and steward certain protocols/methodologies such as the carbon sequestration protocol, grassland protocol, blue carbon protocol and methane emissions protocol.

To make it more concrete, last year Regen sold soil carbon credits to Microsoft. These credits were issued using the CarbonPlus Grassland methodology, which not only measures carbon sequestration but also soil health and animal welfare.

With the Regen Ledger v.4, a new marketplace will develop on the Region Network website making it easier for companies and individuals to buy carbon credits and in the future other ecological credits as well.

By having an open accounting and issuance system, we can start to create the basic building blocks necessary for valuing a broader set of assets.

The Balance Sheet must balance

Assets = Equity + Liabilities

We can consider equity to be our natural resources, the natural capital that we have inherited and liabilities as our accrued expenses and long term debt to the planet. This long term debt consists of the exploitation of natural resources and habitats in favour of short term growth. Akin to a perpetual revolving debt that values the end product more than the natural asset with which it was produced. It is not that the financial system intrinsically rewards destruction over regeneration and protection, just that until now there was a small or even no price to destruction.

Capitalism so far has dramatically increased our liabilities and eroded our natural equity in the process. The balance sheet does not balance because our equity was not properly valued.

Tokenising ecological assets can create a market for protection and regeneration, giving it a clear value that can be accounted for.

These assets are a new investment class that can drive behavioural incentives to more accurately price the equity part of Nature’s Balance Sheet. Regen Network facilitates the creation of these assets and thereby positions itself at the forefront of the blockchain and carbon sector; two growing industries. Moreover, in contrast to other more established sectors, the carbon market is still young and ripe for new technological integrations.

Final thoughts

Fighting climate change and establishing healthy ecosystems does not have to be charity, it can actually be a good investment. We are creating new ways of accounting and measuring ecological state changes, these changes can be tokenised and valued at market. Such states are representative of other systems in growth or decline like a Nation’s GDP.

Some readers at this point may be wondering whether this means a financialization of earth’s ecosystems and whether the inevitable financial derivative of a land in the Amazon is a good idea. I’d argue that this has already happened except the derivatives value lies not in protection or growth of the land but in its decline and destruction, as the perishable end product is more valuable than the resource used to produce it. The market is blind as to what it values, the only thing it sees are the financial incentives directed towards an outcome. Whether this outcome is sales growth or land growth is irrelevant, provided the growth itself has a market value and a return on investment. Ecological assets will have both.

Thanks to Will Szal, Gregory Landua and Sacha for reading drafts of this thesis.